Weekly Good Reads: 5-1-1

Fear, Macro (over-)valuation, Debt finances, Thinking in Bets, Plastics, "Free Lunch" in Investing

Welcome to Weekly Good Reads 5-1-1 by Marianne O, a 25-year investment practitioner and the author of

on investing, economy, and wellness in an intuitive voice. All the Weeklies are here, and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Please also check out my conversations with Female Fund Managers and Investors - new this year!

Feedback is very important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

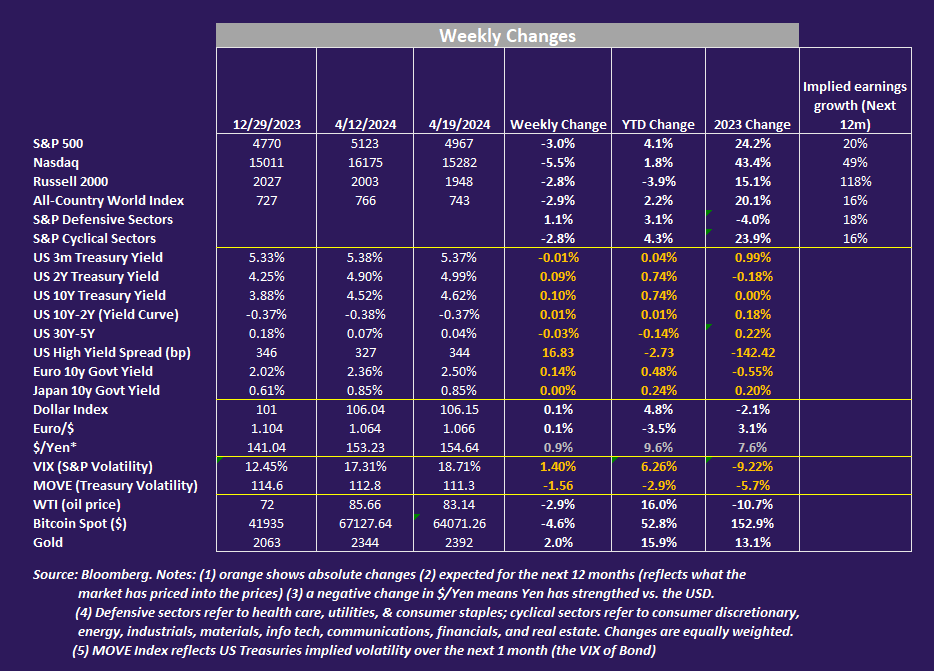

Market and Data Comments

Why did fear fill the market when the underlying US economy is strong (see strong March advanced retail sales and industrial production)? The CNN Greed and Fear Index as of the close of 4/19 was 31 (out of 100), approaching extreme fear, mainly driven by heightened stock, bond, and stock options volatility and haven demand.

From the chart below, haven demand including gold, Swiss Franc, and Yen have ticked up since March beginning, with global stock markets dropping every week and stock volatility rising in the past 3 weeks.

Looking at the chart at the top, one key reason is stretched equity valuation in face of economic fundamentals weakening (e.g. rising bond yield and m/m inflation data, higher unemployment rate).

Goldman Sachs found “that the negative effect of worsening economic outcomes on equity returns is larger when the market is overvalued”, and high equity valuation is concentrated on the AI-fuelled tech sector (info tech down 7% for the week, see Weekly Changes below). Rising geopolitical risks added fuel to the fire and rising commodity prices could reignite inflation. With cash yielding over 5%, investors have places to sit out than stocks.

Stock funds redemption reached $21.1 billion in the two weeks through Wednesday, the most since December 2022 (BofA), redemptions from junk bonds were the fastest in 14 months (LSEG Lipper), and Hedge Funds ramping up US stocks shorts the fastest since December 2022 (Goldman).

One key risk of “higher [rates] for longer” (Fed Powell commented on Tuesday it would take longer than expected for the Fed to be convinced to start lowering rates) is the stronger dollar. As economies elsewhere likely cut rates first (discussed in the last Weekly), opening gaps in interest rate differential will boost the USD dollar, hurting the currencies of the developing countries the most (see Econ/Invest #2), leading to imported inflation and more onerous dollar debt payments.

The recent Chinese Q1 real GDP at 5.3% easily beat the official target of 5%, helped by the manufacturing sector (industrial upgrades) and strong exports, but Bloomberg questioned this “magical number”. Reasons include: China has experienced the longest deflationary streak since 1999, and weak retail sales and stagnant household income do not show up in the production-based GDP numbers. The minute data series tell a better picture of China, not the headline numbers.

One more macro news: the IMF in its latest fiscal monitor pointed out nations’ public spending is still 2 to 3 per cent of GDP above the pre-pandemic projections for developing and developed countries (ex-US and China), pushing up interest rates and therefore interest payments. This reflects “the slow unwinding of crisis-era fiscal policies and the introduction of new support measures, alongside new industrial policy measures including subsidies and tax incentives.”

Should countries’ current policies continue, IMF projects about one-third of advanced and emerging economies will see unsustainable public finances, so more decisive efforts by nations to safeguard public finances are necessary.

This coming week, we will monitor the US Q1 preliminary GDP on Thursday and March Personal spending and Core PCE Price Index on Friday, the Euro Area April Composite PMI on Tuesday and ECB Economic Bulletin on Thursday, the Bank of Japan interest rate decision on Friday, and the earnings announcements of more than half of US Tech mega-caps during the week.

Economy and Investments (Links):

Nasdaq Logs Worst Weekly Performance Since 2022 (WSJ or via Archive)

The Nasdaq and S&P 500 have both declined in each of the past three weeks as a stronger-than-expected U.S. economy buoys inflation and scrambles Wall Street forecasts for interest-rate cuts by the Federal Reserve. Those changing expectations are hammering the speculative artificial-intelligence-oriented tech stocks that propelled a market rally in recent months.~WSJ

What Fed’s Rate-Cut Delay Means for US and World: QuickTake (Bloomberg or click here)

The Most Important Global Commodity of the Decade (Mauldin Economics)

Cheap, abundant natural gas is a competitive advantage to US manufacturers. It’s also an elegant geopolitical tool. Producers could export our natural gas to friendly nations (or nations we’d like to be more friendly), while earning a profit by selling the commodity in the global market at higher prices than in the US. Europe needs the US to fill the void left by Russia and the damaged Nord Stream pipeline.~Mauldin Economics

+ Global Economy Remains Resilient Despite Uneven Growth, Challenges - Governments should stay the course on fiscal consolidation amid mounting debt ahead (IMF)

Finance/Wealth (Link):

No Mercy/ No Malice (Scott Galloway)

This piece which came out in 2021 was one of Galloway’s most well-received pieces, and it talks about the difference between having money and being rich, and how to become rich.

Focus on what matters. Be a Stoic in the face of temptation. Use Time to your advantage. Diversify your investments.~Scott Gallaway

+ This is the new magic number for retirement in California — and what it means for you (San Francisco Chronicle or via Archive and mentioned WSJ article via Archive)

Wellness/Idea (Link)

Free Copy of Thinking in Bets LIT videobook (

Substack by )An important idea of this book: saying “I’m not sure” is an essential ingredient for a better decision-maker. I highly recommend watching this video for the highlights of the Book.

We get only one try at any given decision”…“that puts great pressure on us to feel we have to be certain before acting, a certainty that necessarily will overlook the influences of hidden information and luck.~ Annie Duke

One Chart You Should Not Miss: Where Are the Plastics that Are Produced?

In light of Earth Day on April 22, it is pertinent to appreciate some statistics about plastic use and its harmful impact on climate change.

Worldwide production of plastics has risen from 8.3 billion metric tons in the 1950s to 400.3 billion metric tons in 2022 (Statista).

Worse still, as of 2017, 79% of all plastic is sitting in landfills or the natural environment with a small amount incinerated or recycled.

Amongst the various impacts of plastic production on pollution and climate change:

Emissions associated with fossil-based plastics will more than double, and global plastic use is projected to triple, leading to a doubling of plastic leakage to the environment (in the absence of more stringent policies).~OECD

One Term To Know: “Free Lunch” in Investing

Economics Nobel Prize winner Harry Markowitz, the father of “Modern Portfolio Theory”, established in his 1952 seminal research that a portfolio’s risk level is not simply the sum of its components but also depends on how each position interacts (correlates).

Combining different assets with a correlation of less than 1 (meaning an asset does not move in lockstep with each other) can reduce the portfolio’s overall volatility without necessarily reducing the portfolio’s expected returns. A thoughtfully diversified portfolio can have a better risk-adjusted return (measured by the Sharpe Ratio) than its components.

Diversification has therefore been called the “only free lunch in investing”.

Diversification, however, does not always lead to higher risk-adjusted returns. A more diversified portfolio with US and international stocks, US bonds, high-yield bonds, small-cap stocks, commodities, gold, and REITs struggled against a simple 60% US Stocks and 40% US high-quality bonds (60-40 portfolio) in the past 10 years (Morningstar).

First, the correlation coefficients between various assets are not stable and assets tend to rise and fall together in times of crisis. Asset classes such as international stocks and high-yield bonds have a rising correlation with US stocks.

Different macro environments and unforeseen shocks can affect which diversifiers work best. After the Great Financial Crisis of 2008-9 under unconventional quantitative easing, US stocks and bonds have generally fared better than international/emerging stocks and bonds.

The chart below shows a supposedly more diversified portfolio (orange) has lower risk-adjusted returns vs. a 60/40 portfolio (blue).

The 2 charts below show fixed income was a terrific diversifier in times of crashes (1999 Dot.com bubble, 2008-9 Great Financial Crisis, 2020 Pandemic), but in 2022, stocks and bonds both experienced negative returns for the first time since 1977, and commodities and cash were the only diversifiers in a sea of red then.

If you find this a bit abstract, I highly recommend you read this Deepmind research scientist’s take on why diversification is the free lunch using a two-dice stocks example.

Nevertheless, thoughtful and detailed diversification considering the current macro environments across multiple asset classes has a place as assets fall in and out of favour. A truly diversified portfolio selecting from asset classes, countries, sectors, factors, themes, etc. helps reduce overall portfolio volatility and ensures investors do not miss out on global investment opportunities and focus on long-term investing.

Please do not hesitate to get in touch if you have any questions!

Also please check out my latest Conversations with Investment Changemaker

below.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.