Weekly Good Reads: 5-1-1

US Labour Report, China vs. India, Traffic Accidents and Sleep, Total Factor Productivity, Danny Kahneman, Chimpanzees

Welcome to Weekly Good Reads 5-1-1 by Marianne O, a 25-year investment practitioner and the author of

on investing, economy, and wellness in an intuitive voice. All the Weeklies are here, and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Please also check out my conversations with Female Fund Managers and Investors - new this year!

Thank you so much for your support🙏.

Market and Data Comments

A friend asked why the Fed does not just get on with it and start cutting interest rates (so asset prices rise) but tells us dissenting views including possibly “no interest rate cut this year” should inflation stall its cooling (Minneapolis President Kashkari) and “in no rush to cut” (Dallas President Logan).

Unfortunately, the Fed’s mandate does not include asset prices (only stable prices and full employment). This year, disinflation has been bumpier, but inflation has continued its decline. Despite the blowout March US employment report (adding 303,000 jobs vs. consensus of 214,000 making the 3-month moving average at 276,000) and the unemployment rate moving down 0.1% to 3.8%, average hourly earnings grew 0.3% m/m (4.1% y/y), meaning solid but no runaway income growth.

Goldman Sachs explained why we can simultaneously enjoy lower inflation and strong growth. The often-cited reason is that elevated immigration is boosting labour force growth so strong demand growth is matched by supply keeping up. Bloomberg also estimates that the hiring pace can be stronger without inciting wage pressure (see the above chart). Moreover, the unwinding of pandemic dislocations (e.g. inventory rebuilding) overwhelms the impact of any potential retightening of the labour market. Also, the very-lagging official shelter inflation data will continue to drag down core inflation data.

Meanwhile, the global manufacturing cycle (forward-looking global PMI) has turned up to expansion mode and has broadened to manufacturing and services sectors and all regions. The March indicator shows Europe has returned to modest growth while China’s March PMIs, industrial production, and exports all surprised to the upside. China’s manufacturing PMI moved to expansion mode for the first time in 6 months.

This past week’s Fed officials’ “more hawkish” speech and the strong employment report led interest rates to bump up 13bp (US 2Y) and 20bp (US 10Y), with the bond volatility index (MOVE) jumping a whopping 9 points. Global stocks fell about 1% while WTI oil and gold both jumped over 4%.

The market now expects three-quarter point Fed rate cuts, but narrowly at 54% odds from 88.5% odds in mid-February. Note the US inflation-linked (TIPs) market is telling us real yield has risen to a 20-year high. The (real) yield on TIPs is the “total return your TIPS investment will earn above (or below) official U.S. inflation for the term of the TIPS”. When the real yield is high, and when the inflation rate continues to decline, the nominal bond yield can come down. So back to watching the inflation number and not the employment growth number for the Fed’s monetary moves.

This week we will monitor US March CPI and FOMC March Minutes on Wednesday, March PPI on Thursday, the ECB monetary meeting and press conference on Thursday, and China’s March Aggregate financing during the week and CPI and PPI on Thursday.

Economy and Investments (Links):

Speech by Chair Powell on the Economic Outlook and full video including discussion with Powell (@Stanford Business School)

[On why GDP and wage numbers are strong yet inflation is lower]: Some part of that is that there are significantly more people working in the country. But then how does inflation come down? It’s because potential – the capacity of the economy has actually moved up more than the actual output, so it’s a bigger economy but not a tighter one. Really an unexpected and unusual thing.~ Fed Chairman Powell

How Xi Jinping Plans to Overtake America (The Economist or via Archive)

How India Can Win China’s Gold Crown (Bloomberg Originals on YouTube)

+ The Labor Market is Strong ( Stay-At-Home Macro (SAHM))

[On why immigration has been very good for the US]: The big ‘good news’ story of immigration is that immigrants are helping to solve the labor shortages. They are filling jobs that employers have struggled to fill. Early in the recovery, the news was covered with headlines about labor shortages and how they were causing higher inflation via higher wage costs. We don’t see those headlines now. Early in the pandemic, millions of workers left the labor market, especially US-born, many of whom retired or had caregiving responsibilities. The recovery in the US-born labor force was notably slower than the foreign-born. Immigrants were key. ~

Finance/Wealth (Link):

Danny Kahneman, Who Plumbed the Psychology of Economics, Dies at 90 (New York Times)

Before Kahneman and Tversky, people who thought about social problems and human behavior tended to assume that we are mostly rational agents,” the Times columnist David Brooks wrote in 2011. “They assumed that people have control over the most important parts of their own thinking. They assumed that people are basically sensible utility-maximizers, and that when they depart from reason it’s because some passion like fear or love has distorted their judgment.

But Professors Kahneman and Tversky, he went on, “yielded a different vision of human nature.”

As Mr. Brooks described it: “We are players in a game we don’t understand. Most of our own thinking is below awareness.” He added: “Our biases frequently cause us to want the wrong things. Our perceptions and memories are slippery, especially about our own mental states. Our free will is bounded. We have much less control over ourselves than we thought.”~NYT

+ Danny Kahneman: What if Everything is Narrative Fallacy? (Big Picture)

Wellness/Idea (Link)

Jane Goodall Explains What We Can Learn from Chimpanzees and It's a Message the World Needs to Hear (MSN)

She cited that chimpanzees can bring about reconciliation after conflict, a trait humans seem to struggle with more; another one is the exemplary close mother-children relationship with unconditional support, and the other point is not just animals have emotions and personalities like humans, animals’ aggression is a result of impulse and not evilness; only human is capable of evilness.

+ Voices of Hope - Words of Wisdom (short film) (Dr. Jane Goodall and Mercy for Animals)

One Chart You Should Not Miss: Traffic Accidents Casualties in the US By Age and Gender

Thank you to

for this interesting and clear chart for traffic accidents in the US for males and females in 2021, sourced from the World Health Organization Mortality Database. The chart shows drivers in their 20s and seniors have the most casualties.Coincidently, I am reading the excellent book “Why We Sleep” by Matthew Walker. I was blown away by this research on the effect of sleep deprivation on driving — here I quote:

After thirty years of intensive research, we can now answer many of the questions posed earlier. The regular rate of a human being is around sixteen hours. After sixteen hours of being awake, the brain begins to fail. Humans need more than seven hours of sleep each night to maintain cognitive performance. After ten days of just seven hours of sleep, the brain is as dysfunctional as it would be after going without sleep for twenty-four hours. Three full nights of recovery sleep (i.e. more nights than a weekend) are insufficient to restore performance back to normal levels after a week of short sleeping. Finally, the human mind cannot accurately sense how sleep-deprived it is when sleep-deprived.

For every thirty seconds, there has been a car accident somewhere in the US caused by sleeplessness.

You may find it surprising to learn that vehicle accidents caused by drowsy driving exceed those caused by alcohol and drugs combined…drunk drivers are often late in braking, and late in making evasive manoeuvres. But when you fall asleep or have microsleep, you stop reacting altogether…when you fall asleep at the wheel of your car on a freeway, there is now a one-ton missile travelling at 65 miles per hour, and no one is in control.~Why We Sleep

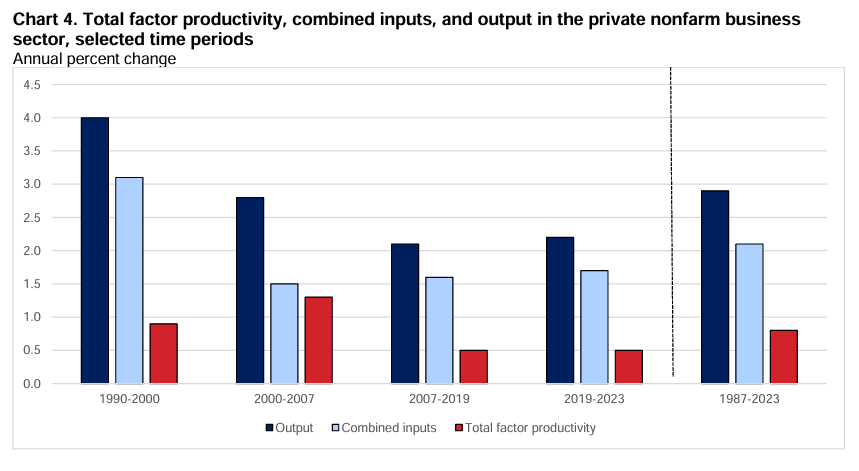

One Term To Know: Total Factor Productivity

According to the US Bureau of Labour Statistics (BLS), total factor productivity (TFP) compares the growth in output over time to the growth in a combination of inputs that include labour, capital, energy, materials, and services. Gains in TFP indicate output growth not a result of an increase in inputs, which means the economy is gaining production efficiency. For example, an economy can produce more without using resources, keeping the nation competitive. An increase in TFP can be due to technological change, organizational changes in the production process, and other efficiency improvements.

TFP is different from labour productivity, which compares the growth in output to the growth in hours worked (not capital and other inputs).

For 2023 (see chart below), total factor productivity increased by 0.7% (output of 2.6% minus combined inputs growth (capital input, hours worked, and labor composition) of 1.9%).

On a longer-term perspective, the 0.7% TFP in 2023 is in line with the range in 1987-2023, much higher than 2007-2019 and 2019-2023 but much lower than the fast TFP growth period of 2000-2007.

Please do not hesitate to get in touch if you have any questions!

Also please check out my Conversations with Female Investors and other changemakers.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.