Weekly Good Reads: 5-1-1

"Dovish" Central Banks, Japan, Dot Plot, US Household Net Worth, Stock Market Drivers, FDI, Friends in Marriage

Welcome to Weekly Good Reads 5-1-1 by Marianne O, a 25-year investment practitioner and the author of

on investing, economy, and wellness in an intuitive voice. All the Weeklies are here, and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Please also check out my conversations with Female Fund Managers and Investors - new this year!

Thank you so much for your support🙏.

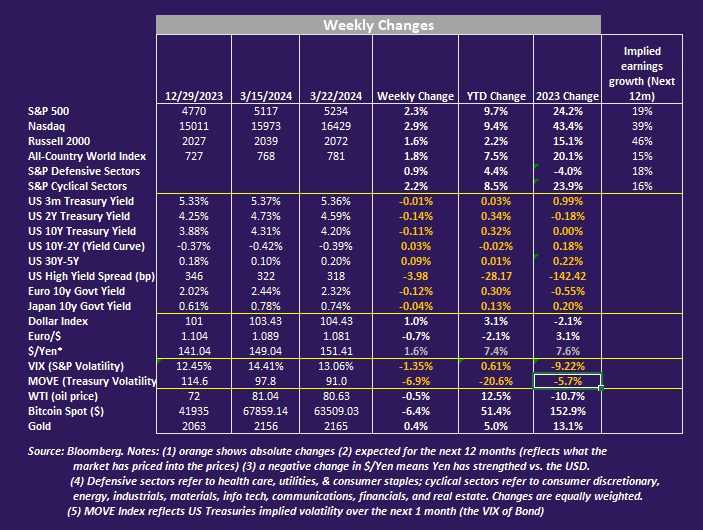

Market and Data Comments

Yields were down, stocks had a good run (especially growth and cyclical sectors), high yield spread dropped, and volatility (equities and bonds) fell, thanks to the dovish tone of the central banks around the world this week.

Japan finally exited its negative rate policy and yield curve control and returned its policy rate to the overnight call rate while continuing to buy JGB (government bond) to ensure no spikes in the long-term interest rates.

Read

by Jesper Koll for his detailed analysis of what to come for Japanese macro policies as he said Japan will “begin to focus on containing rising inflation risks.”

The Swiss National Bank became the first developed market to cut interest rates (by 25bp) declaring its fight against inflation has been effective in the past 2.5 years. Bank of England and ECB also leaned towards cutting rates in June, while central banks in Brazil and Mexico continued their rate cuts. Turkey and Taiwan surprised the market with interest rate hikes.

In the Fed’s March 2024 Summary of Economic Projections, the median dot plot of Fed Funds projection still implies 3 interest rate cuts this year (median Fed Funds rate at 4.6% at the end of 2024 compared to 5.25-5.50% currently). The median tendency of the dots, however, rose 25bp in both 2024 and 2025 and shifted higher for the longer term, indicating the neutral rate may be higher in the Fed’s mind. (The neutral rate is the elusive rate at which the economy operates at full employment and capacity and a steady inflation rate.) (Here’s a more detailed explanation of the Dot Plot).

The Fed, following the stronger-than-expected growth and labour market data, revised its GDP projection and inflation rate upward for 2024 (see table above). Powell remained open for interest rate cut(s) this year, likely starting in June or July, supported by Powell’s repeated saying that they will get long-term inflation back to 2% (estimated in 2026).

In China, industrial production, fixed asset investment, and exports grew faster than expected in Jan-Feb but retail sales growth slowed and property market indicators continued to turn down. The preferred policy tool to ease policy remains interest rate cuts rather than fiscal stimulus, but this cut may need to await after the Fed rate cut begins.

As the stock market party continued, it is good to remind ourselves of the fast decline in the implied equity risk premia globally as higher bond yields set in (equity risk premium (ERP) is the cost of equity minus government bond yield). US’s ERP is now down to the level of 2007 to 2008, indicating there is a much less margin for error.

In the coming week, we will monitor the US Q4 real GDP on Thursday, February personal spending, and February core PCE price on Friday and the preliminary March inflation rates for Spain, Italy, and France.

Happy Good Friday!

Economy and Investments (Links):

Switzerland Kickstarts Rate Cuts for Major Central Banks (AFP)

Pumped Stock Investors Look Beyond US Mega Tech: Macro View (Bloomberg terminal)

Antitrust Suits Leave Big Tech Unbowed (Axios)

The bottom line: Glacial antitrust trials have done little so far to limit the wealth and power of tech's biggest companies. The newest addition to the litigation onslaught faces similarly long odds. (Axios)

Finance/Wealth (Link):

So Much Money Everywhere (A Wealth of Common Sense)

The net worth of Americans hit another new all-time high by the end of 2023. And sure, debt levels have hit new all-time highs as well but assets are growing at a much faster pace [household assets to liabilities is 8.6x as of end of 2023 vs. 7x in early 2000].

+ Stop Loss (@Friday Forward) - a very important discipline in investing!

Wellness/Idea (Link)

Can a Friend Be Your Most Significant Other? (Vox)

…we think about friendship now as a relationship that is kind of an add-on, not necessarily the crux of a good life, and as a relationship that is private rather than one that is publicly recognized or celebrated. And it’s a relationship that’s lower on the hierarchy than family, than romantic relationships, even career.

But if you look back in time, the picture is actually really different. You can go back to the story of David and Jonathan in the Hebrew Bible. You can go back to ancient Roman thinkers and how they talked about their friends as “the other half of my soul,” or “the better half of my soul.” The kind of language that would seem more like what you would say for your romantic partner who is supposed to be at the top of your hierarchy. (Rhaina Cohen via Vox)

One Chart You Should Not Miss: What’s Driving the Stock Market’s Returns?

From Ben Carlson’s blog and this chart based on John Bogle’s book (Bogle is the father of Index Funds), stock market returns are not all speculations but can be broken down into the 3 key components — dividend yield, earnings growth, and change in the P/E multiple (multiple expansion or contractions).

Bogle estimated that:

Expected Stock Market Returns = Dividend Yield + Earnings Growth +/- the Change in P/E Ratio

You will notice earnings growth has been the biggest driver of stock market expected returns except for the two decades of the 1980s and 1990s when multiple expansions dominated.

Note dividend yield for the US stocks has fallen since the 2000s, dividend has been growing at about 8% per annum (per Robert Shiller’s dividend data) compared to the historical average of 5% per annum.

Therefore, earnings growth and dividend yield/growth have been the key drivers of the US stock market returns. This means fundamental changes have been more important than multiple expansion (speculations) for US stocks.

One Term To Know: Foreign Direct Investments

OECD defines Foreign Direct Investment (FDI) as follows:

FDI is a category of cross-border investment in which an investor resident in one economy establishes a lasting interest in and a significant degree of influence over an enterprise resident in another economy. Ownership of 10 percent or more of the voting power in an enterprise in one economy by an investor in another economy is evidence of such a relationship. FDI is a key element in international economic integration because it creates stable and long-lasting links between economies. FDI is an important channel for the transfer of technology between countries, promotes international trade through access to foreign markets, and can be an important vehicle for economic development. The indicators covered in this group are inward and outward values for stocks, flows and income, by partner country and by industry and FDI restrictiveness. (OECD)

IMF further discussed the benefits of FDI to developing countries:

FDI has become an important source of private external finance for developing countries. It is different from other major types of external private capital flows in that it is motivated largely by the investors' long-term prospects for making profits in production activities that they directly control. Foreign bank lending and portfolio investment, in contrast, are not invested in activities controlled by banks or portfolio investors, which are often motivated by short-term profit considerations that can be influenced by a variety of factors (interest rates, for example) and are prone to herd behavior. (IMF)

Can you guess which country has received the most inward FDI - you probably guessed right:

Recently, the news reported that foreign direct investment, measured by liabilities on the balance of payments statistics of China fell 82% to $33 billion in 2023, reflecting the effect of COVID, geopolitical risks, weak industrial profits, and higher returns/interest rates elsewhere. The top Chinese officials emphasized the importance of wooing FDI back into China in 2024.

Please do not hesitate to get in touch if you have any questions!

Check out also my Conversations with Female Investors and other changemakers.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.