Weekly Good Reads: 5-1-1

American consumption and debt, Chinese stocks rout, Rethinking AI Impact, P/B vs. ROE, Stocks are not the economy

Welcome to Weekly Good Reads 5-1-1 by Marianne O, an investment practitioner and author of

about investing, economy and wellness ideas. Every week I include 5 links to relevant economic and investment, finance and wellness/idea pursuit as well as 1 important chart and 1 term to know. All the Weeklies are here and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.👋 This year, I will share my interviews with female fund managers, investors, founders, technologists and more with the first one below. Subscribe to follow.

Thank you so much for reading and supporting my work 🙏.

Market and Data Comments

What’s to like about the US economy? Stronger-than-expected GDP growth (Q4/Q3 annualized at 3.3% and 3.1% Q4/Q4), a fast-declining core PCE inflation (Fed’s preferred inflation indicator) rising at 2% QoQ annualized (see chart above), unemployment rate below 4%, and non-farm payrolls running likely around 190,000 on a 3-month moving average basis.

Since the Pandemic, American consumers have done much better (thanks to a robust labour market and therefore healthy increase in personal income and spending) than other G10 countries. The share of consumption in US GDP is also huge at 68% compared to 52% for Europe) (see chart below).

The Achilles Heel of the American growth story falls back to the imploding level of debt. From the second reading in Econ/Investments, Mauldin quoted the following passage from the book “This Time is Different” by economists Ken Rogoff and Carmen Reinhart. The US general government gross debt has risen from 53% in 2001 to about 123% in 2023 (IMF).

Economic theory tells us that it is precisely the fickle nature of confidence, including its dependence on the public’s expectation of future events, which makes it so difficult to predict the timing of debt crises. High debt levels lead, in many mathematical economics models, to “multiple equilibria” in which the debt level might be sustained—or might not be. Economists do not have a terribly good idea of what kinds of events shift confidence and of how to concretely assess confidence vulnerability. What one does see, again and again, in the history of financial crises is that when an accident is waiting to happen, it eventually does. When countries become too deeply indebted, they are headed for trouble. When debt-fueled asset price explosions seem too good to be true, they probably are. But the exact timing can be very difficult to guess, and a crisis that seems imminent can sometimes take years to ignite.”

While nothing will be changed in an election year, I am watching the US High Yield Spread (now at 344bp, a 2-year low) for signs of distress in the credit market (see table below).

In Europe, the good news is disinflation is continuing, now below 3% yoy and with weak consumer confidence and lacklustre GDP growth, the ECB will start to cut rates in Q2.

In China, this month’s plunge in all major stock benchmarks including Hong Kong has forced the government to likely mobilize about 2 trillion yuan ($278 billion) from state-owned enterprises to buy shares onshore through the Hong Kong exchange link.

The stock market rout, stalled export growth, falling foreign direct investment, property woes, and low confidence in China/Hong Kong have resulted in two firsts in recent history - China’s GDP nominal growth rate (4.6%) in 2023 dropped below that of the US (6.3%), and China’s nominal GDP as a percentage of that of the US fell from 75% in 2021 to 65% in 2023. The Indian stock market capitalization also exceeded that of Hong Kong for the first time.

This coming week, we will monitor the US FOMC meeting on Wednesday and January non-farm payrolls, wave growth, and unemployment rate on Friday, Q4 GDP estimates of the Euro area on Tuesday, the Bank of England interest rate decision on Thursday, and China’s manufacturing PMI (NBS and Caixin) on Wednesday and Thursday. The market will anticipate big tech earnings with Microsoft, Alphabet, and Apple reporting

Economy and Investments (Links):

Fund Pros Burned in AI Surge Are Giving Up on Active Management (Bloomberg | VettaFI)

Going Bang! (John Mauldin, Thoughts from the Frontline)

What I Learned When I Stopped Watching the Stock Market (Jason Zweig, Intelligent Investor column, WSJ via archive.com)

Finance/Wealth (Link):

Just Buy the F***ing Latte (Founder, Ellevest)

You will hear many complaints from the founder about women being shamed for accumulating debt, shopping, spending, and earning (when they do more housework at home) by society. What to do?

As Gloria Steinem has said, “We will not solve the feminization of power until we solve the masculinity of wealth.” But we’re definitely not gonna solve anything by giving up fancy coffee. Full stop.

A $5 latte (or a $6 or $7 one) isn’t going to ruin your life.

Wellness/Idea (Link):

A List of Reasons Why Our Brains Love Lists (The New Yorker)

But the list’s deepest appeal, and the source of its staying power, goes beyond the fact that it feels good. In 2011, the psychologists Claude Messner and Michaela Wänke investigated what, if anything, could alleviate the so-called “paradox of choice”—the phenomenon that the more information and options we have, the worse we feel. They concluded that we feel better when the amount of conscious work we have to do in order to process something is reduced; the faster we decide on something, whether it’s what we’re going to eat or what we’re going to read, the happier we become.

+ Rethinking AI's Impact: MIT CSAIL Study Reveals Economic Limits to Job Automation (MIT)

The conclusion is striking: a much smaller share of the labor market is at risk of automation than direct estimations based on exposure would suggest. This important result commands a more systematic evaluation of the feasibility of adopting a new technology for an industry, which directly relates to the New Solow Paradox, where firms may fail to adopt an overperforming technology if the barriers are too high.

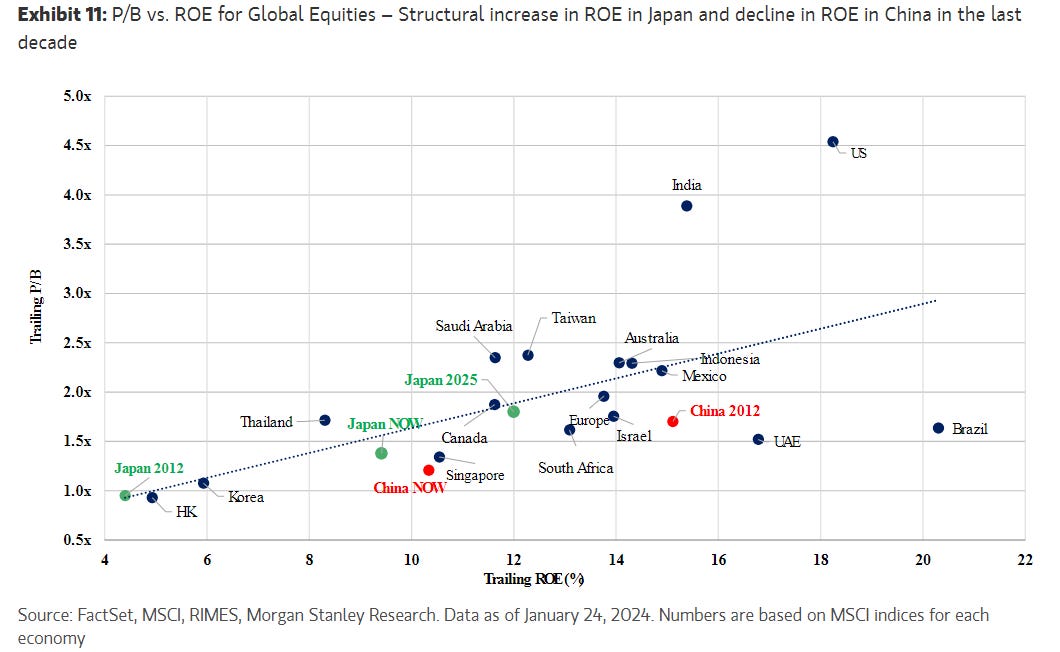

One Chart You Should Not Miss: Price-to-book vs. ROE for Markets - How China’s and Japan’s ROE have Evolved in the Past 10 Years

Here’s a chart that plots a stock market trailing price-to-book ratio against its trailing return on equity. You can see there is quite a good correlation between the two and serves as a quick reference for relative valuation based on fundamentals for investors.

The bullish equity story for Japan hinges on its fast-rising ROE albeit from a very low base (< 5% in 2012) as corporate governance has improved. On the other hand, China’s ROE has gone backwards by almost 5% compared to 2012. (Is the government going to loosen up its grip on the private economy?)

One Term To Know: Stocks Are Not The Economy

The correlation between stock market performance and real GDP growth performance has been unstable in the US in the past 60 years. The 10-year rolling correlations can range from 0.7 to 0 during this time.

If you compare the stock market returns of China (MSCI China Index) and the US (S&P 500) since 1992, China stocks have been flat (!) while the US stocks have grown 2000%, and the US economy grew 300% during this time.

Several reasons can explain why economic growth does not necessarily drive stock performance:

When you compare any periods, the starting point of valuation is key. Multiples can contract from a high level despite positive earnings growth.

Companies’ earnings can grow much faster than the economy and companies can earn a majority of sales from overseas - a case in point is Apple (70%).

Sector composition continues to change within the stock markets - for example, the S&P 500 ‘s technology sector is now close to 30% of the total market capitalization while in countries such as the UK, it is about 1% of the total—a very different driver of market returns.

Still, a prolonged bullish or bearish stock market can affect consumer confidence and the companies capital allocation plans, which will feed back to economic growth.

Please do not hesitate to get in touch if you have any questions! If you like this weekly, please share it with your friends or subscribe to my newsletter.