Weekly Good Reads: 5-1-1

Higher for Longer, Missing Billionaires, Investor Behaviour and Decisions, Oil Prices Impact, PCE

Welcome to Weekly Good Reads 5-1-1, and a warm welcome to my new subscribers! Thank you so much for supporting my work 🙏.

I am Marianne O, an investment professional and author of The Learner’s Mind about investing, economy, and wellness ideas. For this Weekly, I include 5 links to relevant economic and investment news, finance, and wellness/idea pursuit based on what I read. I also include 1 important chart and 1 investment term to know. All the Weeklies are here. You can also find the index of charts and terms. You can easily subscribe to my newsletter by clicking below.

Market and Data Comments

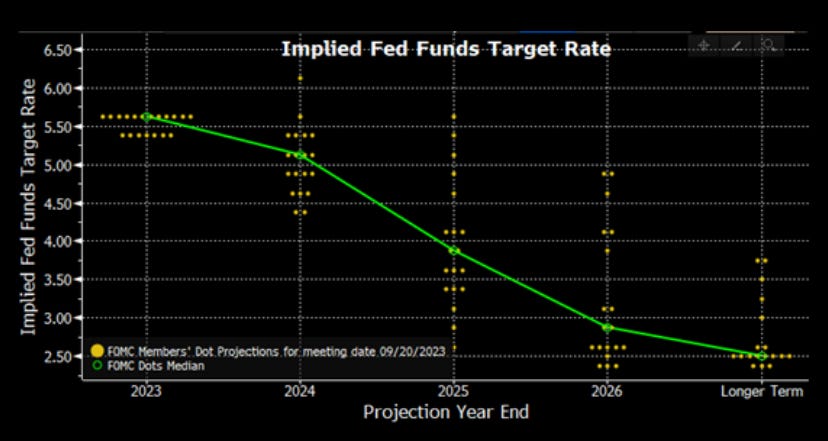

The Fed surprised the market this week not by holding its target interest rate range at 5.25%-5.5% (widely expected) but by raising its GDP projections for 2023 and 2024 to 2.1% and 1.5%. The median dot plot path (green line above) implies fewer rate cuts in 2024 with the Fed Funds rate expected to end at 5.1% at the end of 2024 (compared to the Fed’s June projections).

While the median dot plot of the Fed implies a rate hike of another 25bp before year-end, the market thinks the probability of that happening is less than 50%.

What we know is the Fed is more confident of a soft-landing scenario but not the exact interest rate level as Powell emphasized data-dependency and caution of adjusting rates at this stage of the near-end tightening cycle.

Looming growth threats to the U.S. economy are the expansion of the UAW strike, the possibility of the government shutdown on October 1, and the decline in August existing home sales.

The Bank of England also paused rate hike this week with the governor saying they are “on top of Table Mountain”, implying holding the rates higher (at 5.25%) for longer.

The ECB delivered a 25bp hike this week, and the majority of economists think the hiking is done, citing the lacklustre Eurozone growth.

Stock and bond prices retreated and volatility spiked this week, while major central banks chanted “Higher for Longer” (article #3 under Econ/Investment).

Two pieces of news this week reflect how forecasters and investors can predict returns wrong.

One, the more pessimistic Wall Street strategists finally upped their S&P500 targets after the recent FOMC meeting. Pure forecasters do not have their skin in the game, unlike money managers/investors, who have to keep their customers happy (or make good performances).

Two, this weekend is the 25th anniversary of the failure of LTCM, the large hedge fund that needed Federal Reserve-arranged rescue. What happened? The LTCM investment managers had good ideas but sized up the positions way too large resulting in massive leverage, causing their funds to collapse when their bets went wrong (see Finance/Wealth article link about making better financial decisions).

Next week, China goes on holiday (the Golden Week). We will monitor the ECB European Economic Bulletin next Thursday and the US personal income, personal spending, PCE, and core PCE index next Friday (read One Term to Know below).

Economy and Investments (Links):

Rates Are Like Mountains. It’s About Getting Down (Bloomberg or click here)

Global Central Banks Unite in 'Higher for Longer' Credo (Reuters)

By this time next year, we anticipate that 21 out of the world's 30 major central banks will be cutting interest rates," Capital Economics wrote in a commentary entitled "A tipping point” for global monetary policy.

~ Capital Economics

Finance/Wealth (Link):

The Greatest Investor You’ve Never Heard Of (George Michaelis) (VettaFi)

Don’t:

Get spooked by volatility. When you own a stock, you own part of an underlying business. “Stocks are much more volatile than the businesses they represent.” We could all benefit from paying less attention to stock price performance and more attention to how the actual businesses are performing.

~George Michaelis, ex-head of Source Capital Capital Stock Fund

Wellness/Idea (Link):

The Puzzle of the Missing Billionaires (TEBI, on a book by Victor Hanghani, the LTCM co-founder)

Over the past century, if the wealthiest families had spent a reasonable fraction of their wealth, paid taxes, invested in the stock market, and passed their wealth down to the next generation, there would be tens of thousands of billionaire heirs to generations-old fortunes today. The puzzle of The Missing Billionaires is why you cannot find one such billionaire on any current rich list. There are a number of explanations, but this book is focused on one mistake which is of profound importance to all investors: poor risk decisions, both in investing and spending. Many of these families didn’t choose bad investments– they sized them incorrectly– and allowed their spending decisions to amplify this mistake.

~Book description on Amazon

One Chart You Should Not Miss: Countries Most (Least) Vulnerable to a $100 Oil Price

Brent Crude Oil almost touched $95 per barrel this week to a 10-month high after chopping around $72 to $77 between May and July 2023.

The Organization of Petroleum Exporting Counties (OPEC) plus Russia’s continued reluctance to supply more oil (extended till the end of the year) and the relatively robust US economy have pushed up oil prices since July 2023, creating more inflationary pressure. Saudi Arabia and Russia supply 40% of the world’s oil. Hedge funds are betting oil prices will rise above $100.

From the chart below, Europe, China, India, and Japan are vulnerable to higher oil prices as they lack crude energy resources. They need to pay close attention to improving economic resiliency.

Countries such as Saudi Arabia, Norway, Canada, and Australia are beneficiaries of higher oil prices. The US has relatively diversified energy sources despite its massive oil demand.

One Term To Know: Core PCE/PCE versus CPI

PCE stands for Personal Consumption Expenditure. It is the broadest measure of inflation in the US, accounting for over 60% of economic activity. It measures the prices that consumers (all households and non-profits that serve these households) pay for goods and services, both domestically produced and imported. It is a broader measure of inflation than CPI (tracks urban households only) and uses different weights to calculate inflation.

Core PCE excludes food and energy prices as these two categories tend to be more volatile than other prices and can obscure the underlying trend in inflation. Core PCE is more closely correlated with long-term inflation expectations than overall PCE. PCE and core PCE are useful measures of inflation: they are comprehensive, timely (released monthly), and regularly reweighed.

Why does the Fed use core PCE rather than CPI inflation as its key inflation indicator? Core PCE is a more stable measure of inflation (less affected by short-term price changes). The Fed's primary goal is to maintain price stability, which it defines as a low and stable inflation rate.

Please do not hesitate to get in touch if you have any questions! If you like this weekly, please share it with your friends or subscribe to my newsletter.

Great post!! Really like your substack.