Weekly Good Reads: 5-1-1

Inflation risk, China's deflation, Not 10,000 steps, Yield Curve Steepening, US-China Decoupling

Welcome to a new issue of Weekly Good Reads 5-1-1, and a warm welcome to my new subscribers! Thank you so much for joining and supporting my work 👐🙏👐. Please let me know any feedback or questions by commenting below.

I am Marianne O, an investment professional and author of The Learner’s Mind about investing, economy, and wellness ideas. For this Weekly, I include 5 links to relevant economic and investment news, finance, and wellness/idea pursuit based on what I read. I also include 1 important chart and 1 investment term to know. All the Weeklies are here. You can easily subscribe to my newsletter by clicking below.

Market and Data Comments

Each week I include a table like the one below showing the weekly changes in the major market benchmarks so you can have a quick idea of what has been happening in the financial markets.

This week the global stock market declined, and bond yields rose (except for Japanese bonds). The best-performing segment in the S&P 500 was the defensive sectors, which comprise healthcare, utilities, and consumer staples stocks, while tech stocks retreated and massive Treasury bond issuance caused bond yields to rise.

US July CPI and wage data were soft (core services inflation rose, but core goods inflation declined as seen in the chart above) even though the Producer Price Index (PPI) ticked up 0.3% mom in July compared to 0% mom in June due to an exceptional jump in the portfolio management fee.

Shelter inflation (rents, lodging, hotels, home insurance) accounted for 90% of the US CPI monthly (modest) gain in July. Overall, CPI, wage, and job data are moving in the right direction.

Earlier in the week, the New York Fed President noted the real interest rates (proxied by Fed Funds rate minus the 12-month inflation expectations) are above neutral now, but there is no need to be so far above neutral next year. As inflation expectation is expected to decline from about 3.3% to 2.4% by end-2024, interest rates can fall by about 1% to 1.25% next year (Morgan Stanley). See El-Erian’s * article below for the caveat.

China is experiencing first-time CPI deflation, which helps the price trend globally. CPI fell 0.3% yoy, and PPI fell 4.2% yoy, its 10th consecutive month yoy decline as the property market slump has hurt domestic confidence and consumer spending.

China’s youth urban unemployment rate in June 2023 was 21.3% (and 46.5% if those not in education, employment, or training are counted), leading to the proliferation of “professional children” or those “chewing on the elderly.” Granted, many of these youngers have university degrees or family support. Strategic technology development and public-private enterprise corporation as in the “Heifel Model” have emerged as a new source of growth.

Next week, watch for Q2 Japan real GDP, China July retail sales, industrial production, and investments yoy change, US July retail sales and housing starts, UK July CPI, and the release of FOMC meeting minutes.

.

Economy and Investments (Links):

Good News on Inflation Comes With an Asterisk (Mohamed El-Erian, Bloomberg News)

China Slips Into Deflation in Warning Sign for World Economy (WSJ)

Behind The Curtains of Buffett's Life with Alice Schroeder (@Neckar Substack)

It’s a delicate balancing act as excess liquidity continues to be supportive of risk assets for now. But once the inflation data is showing clear signs of rising, it will already be too late to get ahead of the selloff.

Markets may be most wrong at economic turning points, but nobody said detecting them in real time would be easy. Nevertheless, being aware one is coming is the sort of good fortune that favors the prepared.

Bloomberg’s MacroScope column

Finance/Wealth (Link):

The (In)Accuracy of Market Forecasts (Wealthmanagement.com)

The conclusion and the importance of forming your conviction you are comfortable with:

One of the most interesting, and surprising, results is that despite their greater financial literacy, the professional forecasters produced significantly worse forecasts than the average household. The takeaway is that market forecasts should be ignored, regardless of whom they come from—professional economists or market gurus. Instead, investors are best served by having a well-thought-out plan, including rebalancing targets, and sticking to that plan. That’s the warning Warren Buffet offered in his 2013 letter to Berkshire shareholders: “Forming macro opinions or listening to the macro or market predictions of others is a waste of time. Indeed, it is dangerous, because it may blur your vision of the facts that are truly important.”

Wellness/Idea (Link):

Forget 10,000 Steps. Here's How Much Science Says You Actually Need to Walk (Time Health)

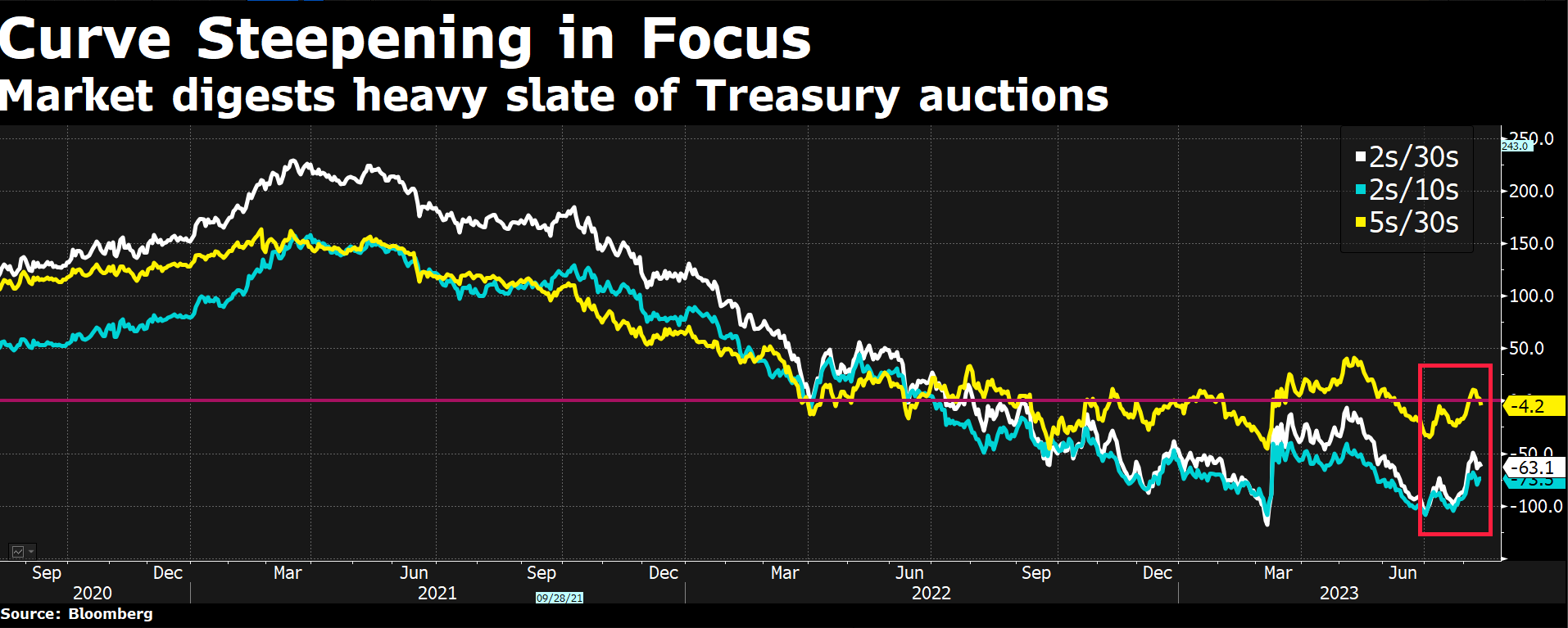

One Chart You Should Not Miss: US Yield Curve Steepening

The yield curve (proxied by the 10y government bond yield minus the 2y government bond yield) steepens when the yields on long-term bonds rise faster than yields on short-term bonds or when short-term bond yields fall as long-term bond yields rise.

Usually, this is because investors expect faster economic growth, higher inflation, and therefore higher interest rates.

Currently, the US is experiencing an inverted yield curve where the 2y yield is higher than the 10y yield, but the yield curve has steepened since the end of June, which means investors need higher compensation to hold longer-term securities. A sudden steepening of the yield could signal the onset of recession, which the market is closely watching.

One Term to Know: US-China “Decoupling”

It is the gradual reduction of the economic interdependence between China and the US in trade. China’s share of the overall US trade deficit ($1 trillion in 2022) has fallen from 47% in 2018 to 32% in 2022. US-China bilateral trade in goods and services was 3% of US GDP in 2022 versus the peak of 3.7% in 2014 (Project Syndicate).

Factors for trade decoupling include the need to reduce dependence on a foreign country on the supply of critical technological products, facilitation of domestic dominance of indigenous firms, trade tariffs, rising country tensions, etc.

The US has restricted exports to China technology producing advanced computing chips and supercomputers, and likely AI chips in the name of “de-risking”.

Lately, Treasury Secretary and others in the Biden administration warned that “a full separation of our economies would be disastrous for both countries.”

Please do not hesitate to get in touch if any questions! If you like this weekly, please share or subscribe to my newsletter.