Weekly Good Reads: 5-1-1

Inflation reality, AI ETFs, long-term investing, QT, 3-or-4 hours work

Welcome to another issue of 5-1-1! I am Marianne O, an investment professional and author of The Learner’s Mind on investing, economy, and wellness ideas. For this Weekly, I include 5 links to relevant economic and investment news, finance, and wellness/idea pursuit based on what I read. I also include 1 important chart and 1 investment term to know. You can easily subscribe to my newsletter by clicking below.

Market and Data Comments

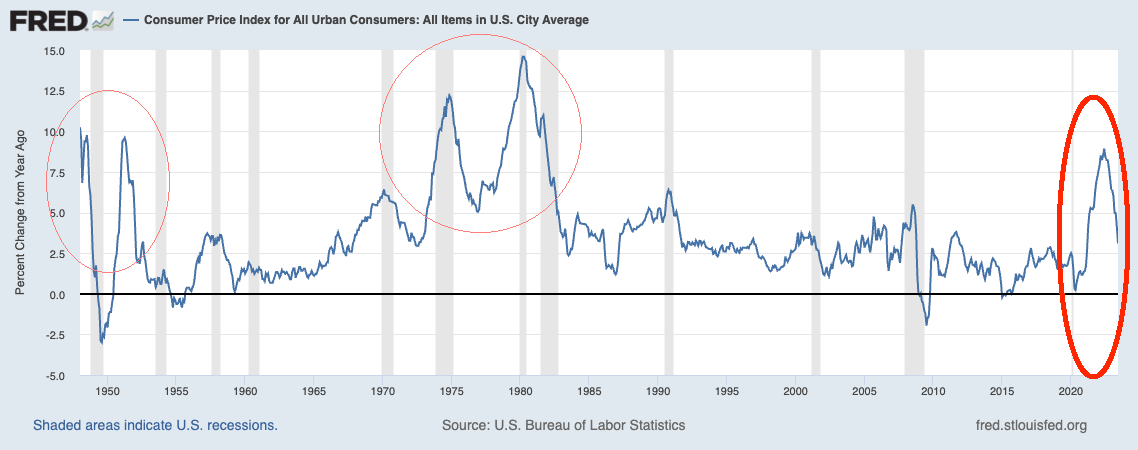

The US Bureau of Labor reported June CPI was 2.97% yoy (the lowest in two years) vs. the peak of 9.1% yoy in June 2022. Core inflation rose less than expected at 0.16% mom albeit at 4.8% yoy. Producer prices (PPI) rose slower than expected at 0.1% yoy, the smallest rise since 2020. Markets saw this as the emergency is over—US stocks climbing 2.44%, the dollar index falling 2.3%, and 2y and 10y government bond yields rallying 18bp and 24bp respectively this week.

Commentators called for the Fed to stop raising rates NOW.

(in It’s Time to Declare Victory in the Inflation Flight) highlighted government monetary and fiscal policies have reduced labour income inequality (raising the lower-wage workers).Barry Ritholtz (Big Picture, see article below) pointed out the Fed has driven inflation HIGHER by raising rates because the main drivers of current inflation have been apartment rental costs, shortage of homes, and too few workers. Hiking rates do not solve these problems.

The good news is, according to

, the new and key disinflation indicator called New Tenant Repeat Rent Index, which lags the official rent CPI by about one year, is in deflation now.

However, the Fed will likely focus on the stickiness of non-housing services inflation (aka ‘supercore’, which is over 50% of the core PCE inflation and the Fed preferred inflation measure), so the July interest rate hike is still on the table.

While the US enjoys the Goldilocks scenario where the economy is neither too hot or too cold (do not get in the way of a soft landing narrative), China has been flirting with deflation (June: 0% yoy) and a substantial decline in exports by -12.4% in June (imports fell 6.8%).

With the real estate downturn, economists cautioned on China's ‘Japanification’ risk. The government has recently put a brake/stop on fining Big Tech, welcomed foreign investments, and urged the local governments to support tech firms.

Meanwhile, US big banks lending income (JP Morgan, Citi, Wells Fargo), especially consumer credit, is growing, allowing their earnings to beat expectations. However, next week regional banks’ earnings will tell another story.

When the CNN Greed and Fear Index has been flashing greed for over a month and my hairdresser commented to me the stock market is rising high, you know what to do - take caution!

Next week, we will monitor China's Q2 GDP, retail sales, and industrial production on Monday, US retail sales on Tuesday, Japan's CPI on Friday, and the G20 finance chiefs/central bank governors meeting in India.

Economy and Investments (Links):

A Dozen Contrarian Thoughts About Inflation (Big Picture)

Quant Firm AQR Spots Deal of the Century in Emerging Markets (Bloomberg)

The market has $11 trillion worth of ‘Magnificent 7’ questions. Bank of America has the answers (MarketWatch)

How can equity investors navigate these risks? Look beyond the Mag 7.

“Equity opportunities are likely to broaden beyond the seven stock cohort. Valuations are more attractive outside of these companies, and projected returns based on consensus are higher for the equal-weighted S&P 500,” says Subramanian … We would avoid crowded, expensive tech companies with ailing share gains. But tech companies with healthy balance sheets capturing and/or retaining market share leadership should be considered for a core holding.”

~ Savita Subramanian, strategist at Bank of America

Finance/Wealth (Link):

AI and Other “Mega-Forces” Are Reshaping Markets. How to Play Them with ETFs (Barron’s)

Related: Josh Wolfe (Lux Capital) on Where Investors Will Make Money in AI (Bloomberg Odd Lots Podcast)—this is a solid discussion about the future of AI (e.g., genetic data - biology, in-person communication away from AI voices, or prompt engineering.)

Wellness/Idea (Link):

The Three-or-Four-Hours Rule for Getting Creative Work Done (Oliver Burkeman)

Bonus: Cartoons About Therapy from the Past Century (Well, Almost) (The New Yorker)—cartoons never fail to relax me, and I hope they do for you, too.

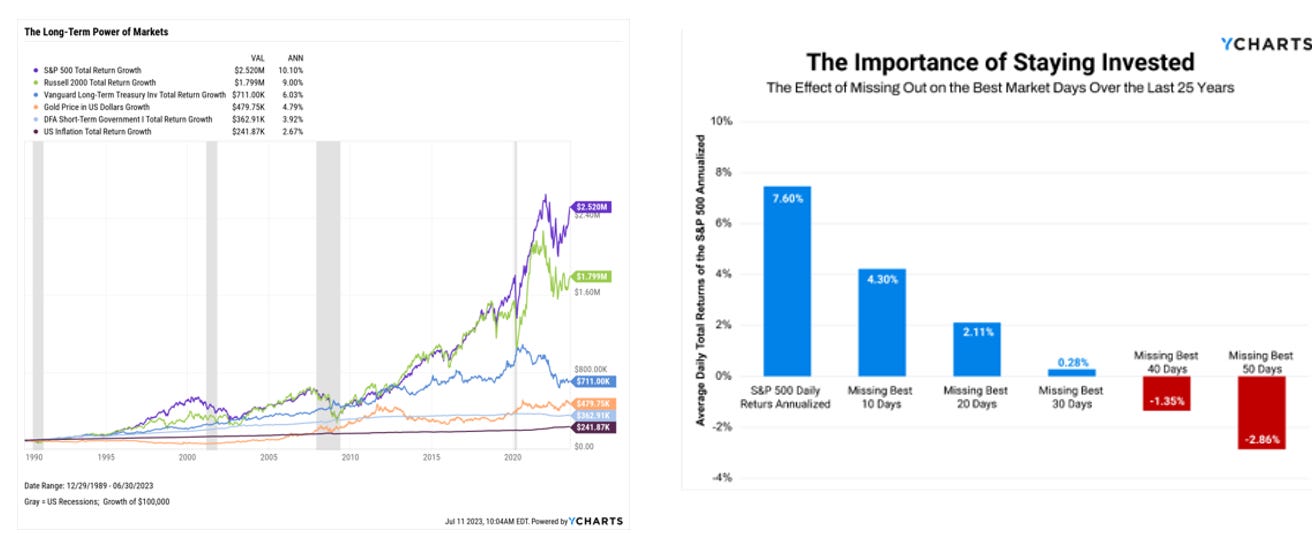

One Chart You Should Not Miss: The Long-Term Power of Markets

The chart on the left from YCharts shows the growth of a $100K investment over 30+ years (1990 through Q2 2023).

Look at the ANN column which shows the annualized return for each asset type over 30 years.

The chart on the right shows the impact of missing out on the best market days when investing in the S&P 500 Index over the last 25 years. If one tries to time the market, instead of earning closer to 8% a year, one could lose about 3% a year.

Which strategy would you choose?

One Term to Know: Quantitative Tightening (QT)

Quantitative tightening or balance sheet normalization (after quantitative easing) refers to the reduction of the Federal Reserve balance sheet (both assets and liabilities). On the asset side, the Fed holds Treasuries and mortgage-backed securities. The liability side consists of the currency held by its citizens and funds held by the banks parked at the Fed (bank reserves).

Reduction of balance sheet works with rising interest rates to tighten monetary policy (see chart below).

The Fed’s balance sheet ballooned to $4 trillion after the 2008 financial crisis. After the slow decline from 2017 to 2019, the Fed did QE again to buffer the shock of the Pandemic. The balance sheet reduction resumed in April 2022 except for the bump up around March 2023 due to the regional banking crises.

The Fed plans to reduce its balance sheet over several years while maintaining the objectives of maximizing employment and stabilizing prices. It can sell securities outright or stop reinvesting the securities when they mature.

Please do not hesitate to get in touch if any questions! If you like this weekly, please share or subscribe to my newsletter.