Weekly Good Reads: 5-1-1

On U.S. Jobs, China's local debt, ex-AI trends, and Swedish Fika

Welcome to another issue of 5-1-1! I am Marianne O, an investment professional and author of The Learner’s Mind on investing, economy, and wellness ideas. For this Weekly, I include 5 links to relevant economic and investment news, finance, and wellness/idea pursuit based on what I read. I will also include 1 important chart and 1 investment term to know. You can easily subscribe to my newsletter by clicking below.

Market and Data Comments

The U.S. averted debt default, and the debt ceiling was suspended (not raised) until January 2025, allowing the government to keep borrowing and paying bills on time before then. NYT expects the budget spending to be cut by $136bn in the next 2 years. But credit agency Fitch Ratings put the U.S. on credit watch, citing a steady deterioration in governance and the U.S. inability to deal with fiscal challenges.

This week’s main market themes were AI-induced growth (tech) stock rally and renewed job market strength (May job add was 339,000.) The 6-month moving average of payroll gains increased for the first time since October 2022 although the unemployment rate ticked up from 3.4% to 3.7% while the average weekly hours worked fell slightly.

The economy will face a less stimulative U.S. fiscal policy and a more restrictive monetary policy going forward. Economists estimated financial conditions have evolved in a way equivalent to a 75bp rate hike since mid-May. The Fed may skip the June rate increase. The Fed also has already re-anchored the market’s long-run inflation expectation (@apricitas economics). Read

’s Substack for a dissection of current economic topics.Two other trends and potential risks are worth investors’ attention. Asian investors rated the burgeoning Chinese local government debt, which finances public infrastructure and property market, at the top of Asian market risks (see chart below). Expects more property market support measures to come in China. The other concern (over the long run) is the collapse of the global fertility rate (see the Economy/Investments section).

“…whereas the rich world currently has around three people between 20 and 64 years old for everyone over 65, by 2050, it will have less than two. The implications are higher taxes, later retirements, lower real returns for savers and, possibly, government budget crises” (Economist).

Next week’s important events include OPEC’s meeting on June 4 in Vienna (bullish or bearish oil market outlook?) and Apple’s most significant product launch in a decade, which includes mixed-reality headsets.

Economy and Investments:

Backlash Against Weaponized Dollar Is Growing Across the World (Bloomberg)

The $1 Trillion Company That Started at Denny’s (WSJ Audio, with transcript)

How the Value Trade Has Been Smoked by the AI Frenzy (Bloomberg)

Bonus: Global fertility has collapsed, with profound economic consequences (The Economist or here)

Finance/Wealth:

It’s Not Just AI. 5 Trends That Will Change How You Invest (Barron’s or view here)

Wellness/Idea:

The Swedish tradition that can make you happier at work (BBC video)

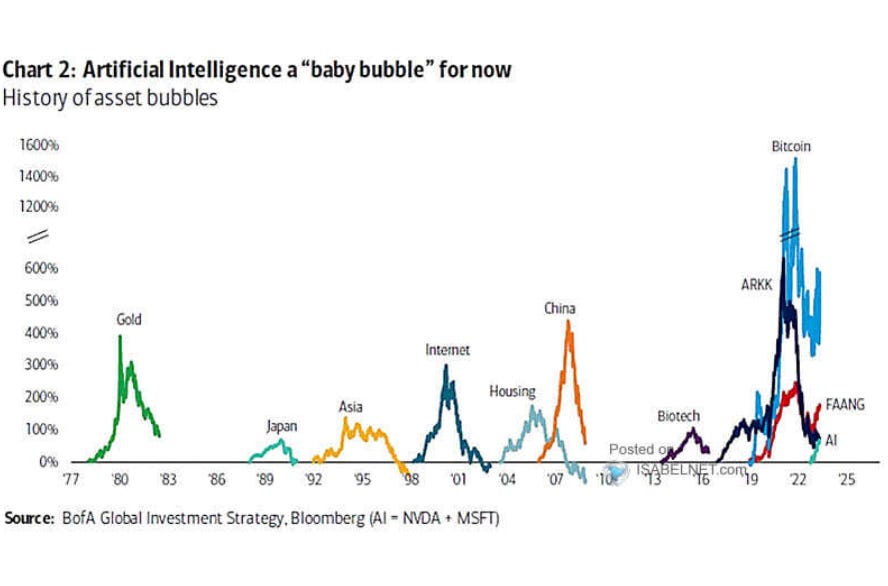

One Chart You Should Not Miss: History of asset bubbles

If you are worried about AI-themed investing being in a bubble, take a look at Bank of America’s chart showing a history of asset bubbles since the 1970s. Compared to the internet boom and bust, the AI boom is a baby one and appears to have lots of runways (no, this is not a Tulip bubble like the 1630s).

One Term to Know: ETF Creation and Redemption Process

This is a unique feature of ETF, allowing the ETF to track the value of the underlying basket of securities tightly and making it cost-efficient for investors (note the trading costs are borne by the authorized participants (the broker that creates/redeems ETF shares). In the case of mutual funds, investors have to bear the transaction costs directly. This is one big factor for the rapid rise in the popularity of ETFs in investing.

Please do not hesitate to get in touch if any questions! If you like this weekly, please share or subscribe to my newsletter.